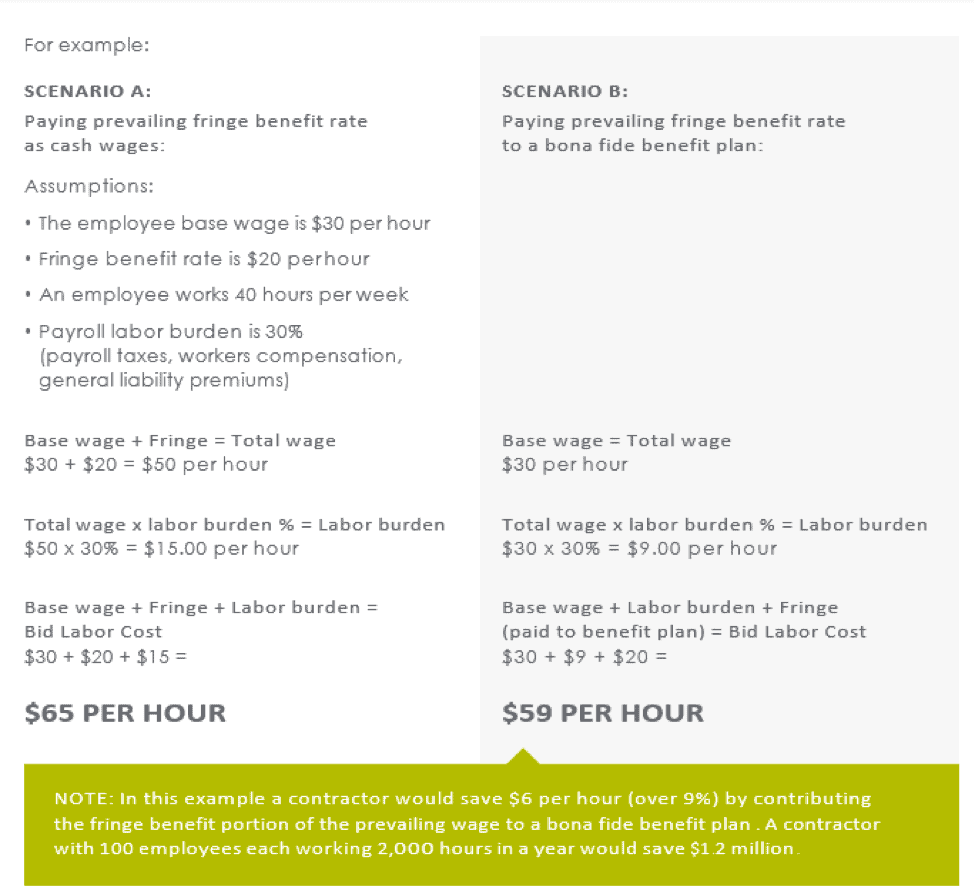

A contractor can choose between providing the prevailing fringe benefit rate as additional cash wages or as bona fide benefits. The cost of paying the fringe rate as cash wages can be expensive since wages are subject to payroll taxes and payroll-based insurance premiums. In most circumstances, this includes FICA, unemployment taxes, workers compensation premiums, and liability insurance premiums. These costs are typically referred to as “labor burden” and can range between 15%–40% of payroll (depending on rates paid for workers compensation and liability insurance).

However, contributions of the prevailing wage fringe benefit rate to bona fide benefit plans are not subject to labor burden cost. This tax advantage can create very large savings for contractors, which can result in more competitive bidding.

Employees also achieve significant savings since contributions to bona fide benefit plans defer (for retirement plan benefits) or avoid (for insurance premiums) income-based taxes.

To calculate how much your company may be able to save by paying the fringe benefit rate to a bona fide benefit plan, visit directadvisors .com/prevailingwage for an illustration .